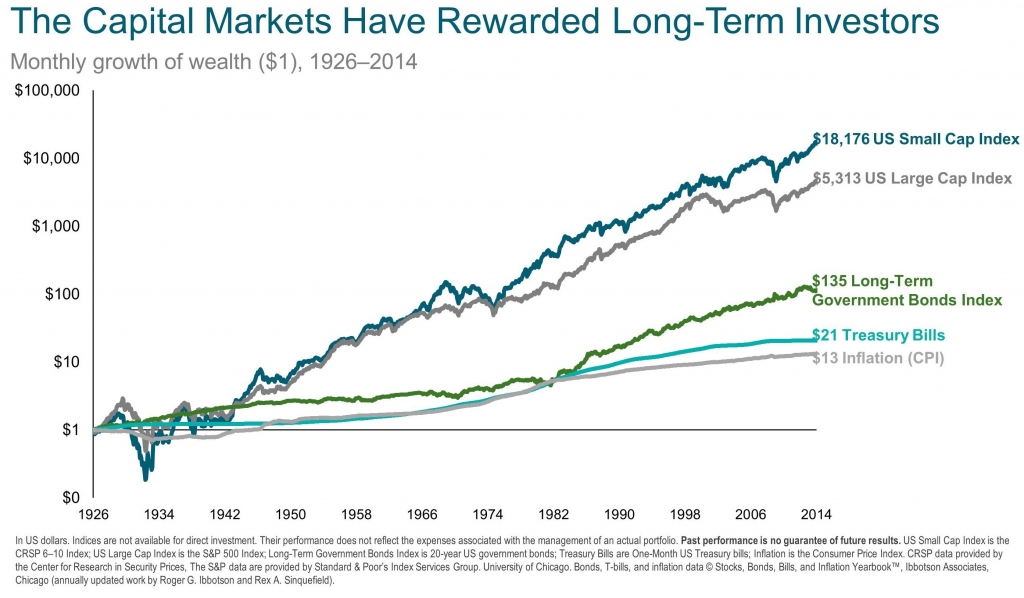

Markets Have Rewarded Discipline

A disciplined investor looks beyond the concerns of today to the long-term growth potential of markets. The chart below shows how $1 invested in 1926 in various asset classes has grown through 2014. The top line shows that $1 invested in small cap U.S. stocks in 1926 would have grown to $18,176 by 2014, which is a full $12,863 more than $1 invested in large cap U.S. stocks over that same period.

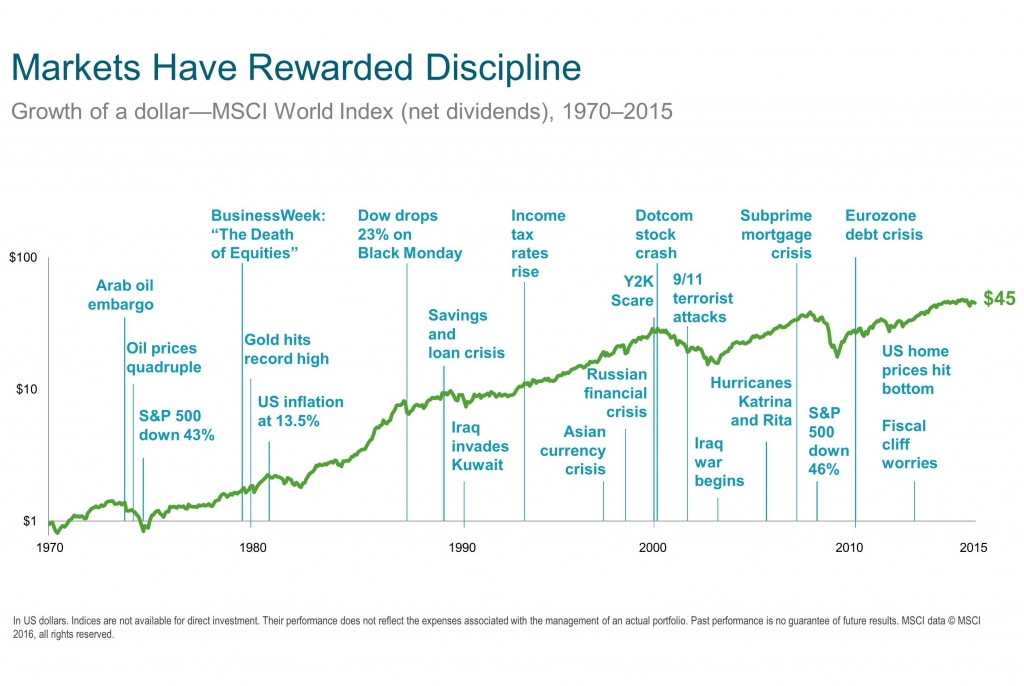

While these lines look relatively straight with only small flickers, we must remember that each small waver can feel like an all or nothing proposition when living through it. The chart below illustrates this point by showing the financial news headlines that have accompanied major market movements of the last 45 years.

While some of the movements may look minor from afar, if you take a closer look you can see how large they actually were in the moment. For example, the S&P 500 Index was down 43% in 1974 and the Dow Jones Industrial Average dropped 23% in one day in 1987. However, the market recovered from these temporary declines and climbed ever higher.

More recently, headlines related to the current market pullback have focused on oil prices and China’s growth. Both of these areas are in transition, and the broader stock markets are reacting to the uncertainty surrounding them. This is not unlike other recent pullbacks when the market was trying to sort out the U.S. fiscal cliff worries and the European sovereign debt crisis. Our opinion is that this too shall pass and the market will regain its footing and climb higher over the long term.

Avoiding Trains (continued)

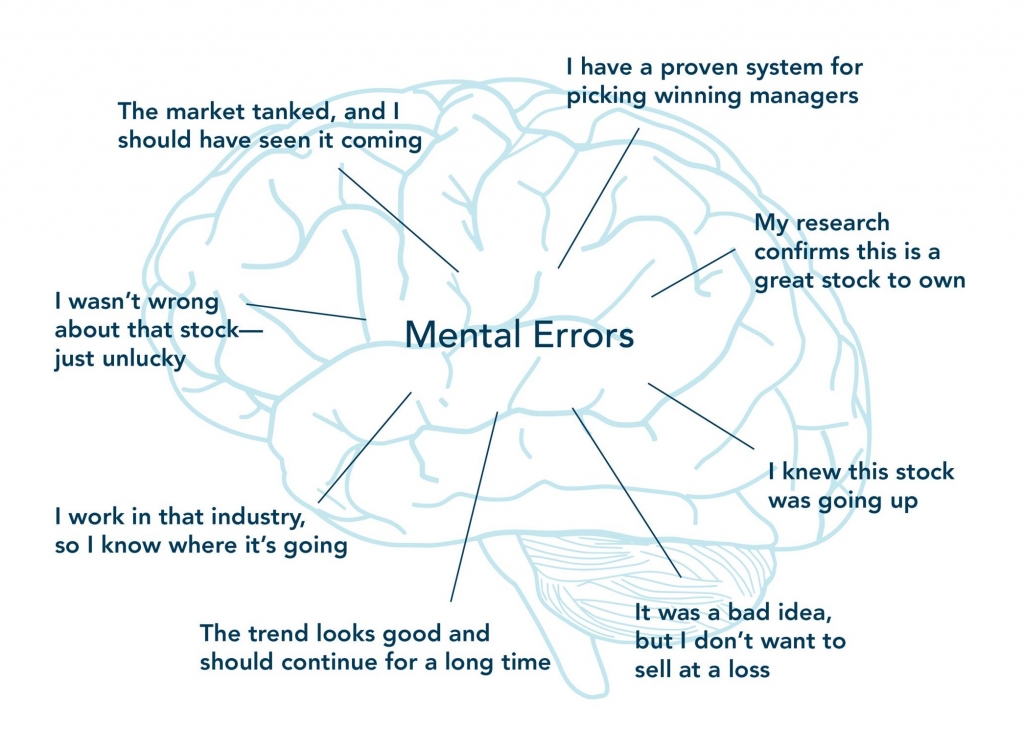

With so much noise in the news and financial press, it’s hard to find a clear “sell” and “buy” signal for the top and bottom of the market. Moreover, research shows that even professional money managers are not good at making these calls.

The reason for this is that humans are not wired for disciplined investing. The research shows that people tend to apply faulty reasoning to investing, when they follow their natural instincts. This is why we follow a structured investment strategy at TAGStone Capital based on years of academic research.

What we do know is that:

1. Markets have historically shown to go higher over time,

2. Certain groups of stocks have shown to outperform others over the long term, but this does not always hold over the short term and it is difficult to pick which groups of stocks will outperform during those shorter periods, and

3. Having an appropriate balance between stocks and bonds provides the means for an investor to stick to an investment strategy, because all investment strategies have periods of relative underperformance.

The last point is reiterated by David Booth, CEO of Dimensional Fund Advisors, in the Barron’s article we have shown many of you before. In the last paragraph of the article, Booth says, “Where people get killed is getting in and out of investments. They get halfway into something, lose confidence, and then try something else. It’s important to have a philosophy.”