Stock Investing at All-Time Highs

As stock markets, once again, continue to hit all-time highs, investors take this news not with celebration, but with trepidation.

Modern stock markets have been worrying investors with new highs since they were created several centuries ago. For example, in 1955, Benjamin Graham, the great teacher of Warren Buffett, was called before Congress to testify about the level of the stock market—and answer the question: “is the market too high.” At the time, the Dow was up 56% from September 1953 to March 1955 and had just returned to its 1929 peak. The Senate committee wanted to ensure abusive actions were not going to create another meltdown—or as the chairman put it, “a final orgy of buying.”

To give a sense of the discussion, below is an excerpt of the statement from Mr. Graham:

"The true measure of common stock values, of course, is not found by reference to price movement alone, but by price in relation to earnings, dividends, future prospects, and to a small extent, asset values.

The Dow Jones industrials are now at a lower ratio to their average earnings in the past than they were at their highs in 1929, 1937, and 1946…. It should be pointed out also that high-grade interest rates are now definitely lower than in previous bull markets except for 1946. Lower basic interest rates presumably justify a higher value for each dollar of dividends or earnings.

Such a figure, if reliable would have to be regarded as rather reassuring. It would indicate that the market in terms of value is no higher now than it was in early 1926, or in early 1936, or late 1946.

It is fair to say the market is not too high today if we really managed to lick the business cycle. Although such a development would involve a revolutionary break with the past, I am not prepared to deny its possibility.

In my view, the fundamental reason for the rise [in the market since September 1953] was the swing from doubt to confidence—from emphasis on the risks in common stocks to the emphasis on the opportunities in common stocks.

My studies have led to the conclusion that sentiment alone, not supported by any visible change in value, will produce a swing on the order of 100 to 250 or 100 to 300 in price.”

An interesting point to note is that the level of the stock market that the senators were so concerned with was the Dow reaching 381. As we know to-day, the Dow crossed 22,000 for the first time on August 2, 2017.

5 Thoughts on the Stock Market (continued)

3. Stock Valuations, in the Long Run, are Related to Corporate Earnings and Cash Flows:

As Buffett’s quote states, stock valuations, in the long run, are related to corporate earnings and cash flows.

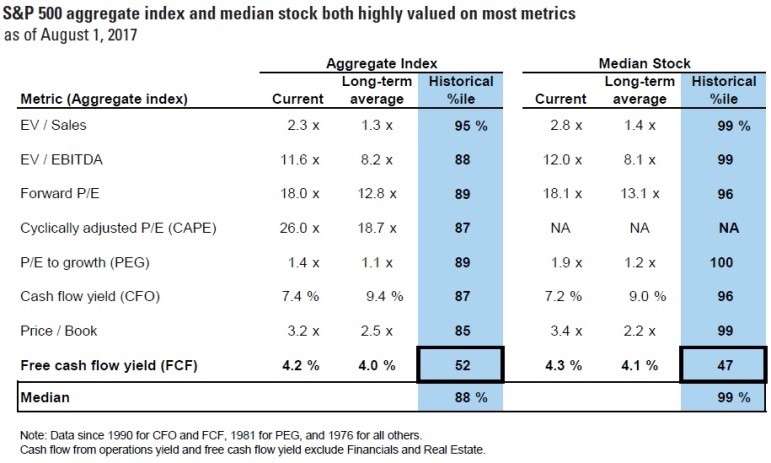

At the present time, the S&P 500 is highly valued by most metrics, but as shown in the table below from Goldman Sachs, the free cash flow yield on the S&P 500 is about 4.2%, almost directly on par with its long-term average of 4.0%, showing that the S&P 500 is fairly valued from this measure.

4. When stocks go down, investors become less inclined to invest, not more inclined:

There is a misguided belief among many investors that they will happily jump back into the stock market once a significant downturn has occurred. “Once we get a 20% downturn, I’ll invest,” goes the thinking.

But during such downturns, fear has usually gripped the market and news headlines are obsessed with how far the market has fallen and how much farther it will go.

Instead of feeling encouraged that stocks are a good buy, investors usually become more cautious, fearing they will put money into stocks only to see the market continue to fall. Instead investors usually continue to sit on the sidelines, waiting until things “calm down.”

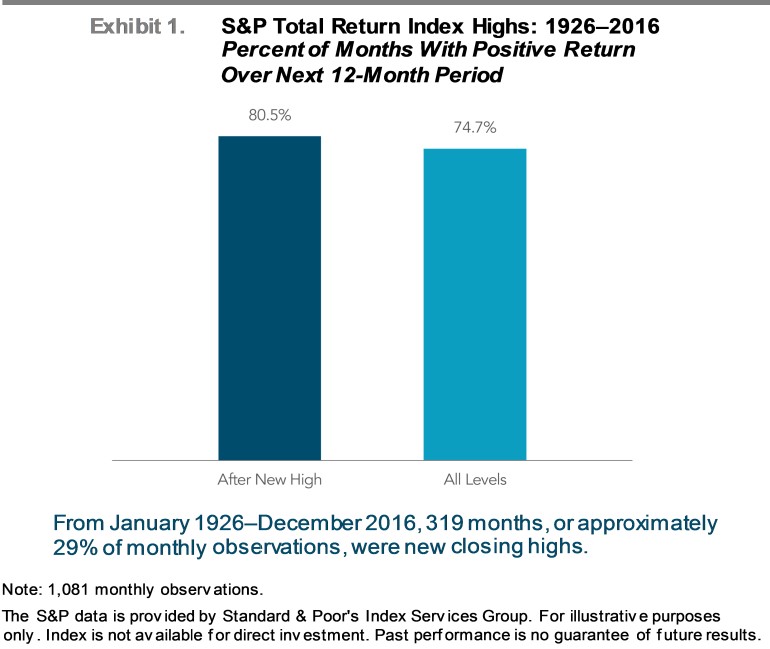

5. Investing Near All-Time Highs is Part of Stock Investing:

Investing near all-time highs is part of stock investing. As shown in the graph to the right, the stock market, from January 1926 to December 2016, has closed at new month-end highs almost 30% of the time.

Historically, however, new highs have not been useful predictors of future returns. As the graph indicates, the chances of positive monthly returns over any 12-month period is about the same, whether the market is hitting a new high or not.