Market-Timing Traps and Temptations

Halfway through the fourth quarter, markets have rebounded from their October lows. While the rebound has provided some relief, there is still a swarm of hand-wringing predictions and “this time it’s different” warnings about what may lie ahead.

As I write this, the S&P 500 is about 3,830, and some top Wall Street analysts have predicted a bear market bottom on the S&P 500 of 3,100. As scary as these numbers are, where the market ultimately bottoms is irrelevant to the long-term investor. For long-term investors, the question is not “What else can go wrong?” but “How much of what can still go wrong isn’t already priced in?”

At 3,830 on the S&P 500, there is a risk that it will go to 3,100 with you fully invested in your desired asset allocation. However, the more significant risk may be that it will go to 5,600—as one day it must—with you still out of it because you held on for the bottom, missed it, and then froze when the market soared. The market can rebound sharply and unannounced after significant declines.

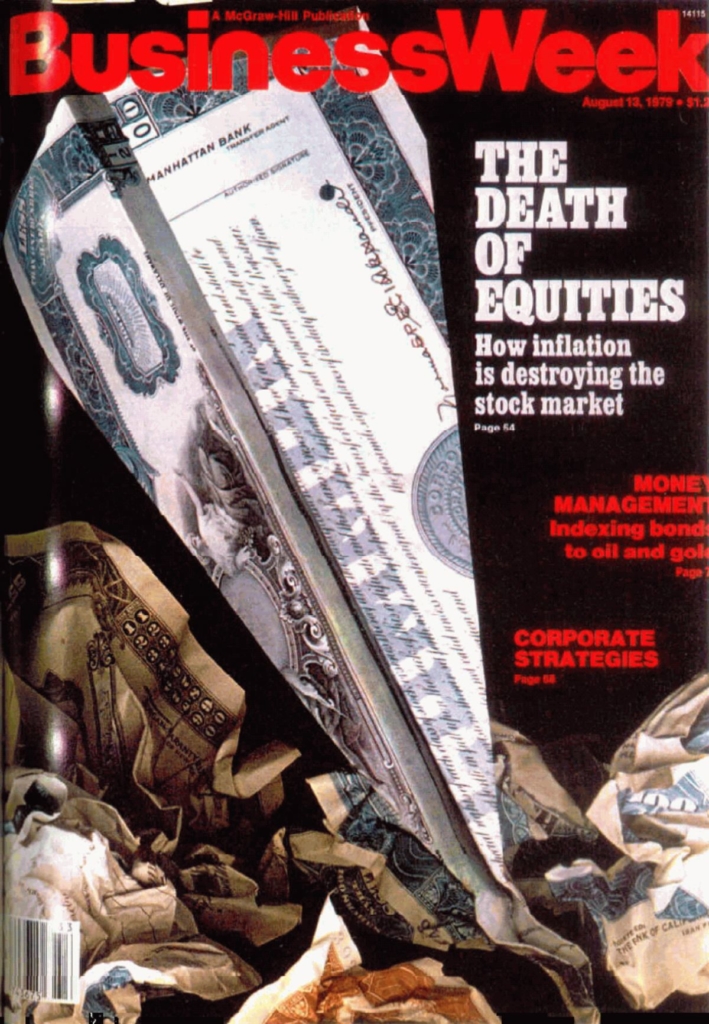

Let’s look at the last time we encountered an inflationary and potentially recessionary economic environment like we’re enduring now. In 1979, BusinessWeek ran the infamous cover story, which declared “The Death of Equities.”

In 2019, reflecting on the BusinessWeek story, a Bloomberg columnist (Bloomberg eventually purchased BusinessWeek) wrote:

“Three years after [“The Death of Equities”] appeared, the stock market hit bottom and then began a remarkable resurgence. The total return on the Standard & Poor’s 500-stock index since its 1982 low, with dividends reinvested, has been nearly 7,000%. Not bad for a corpse.”

It would’ve been a bad idea to give up on capital markets in 1979. It is still a bad idea to give up on them today. Whether the bottom is now or another 20% down, here are a few things to keep in mind:

- If you are holding significant cash for an important long-term goal, it is time to deploy it.

- The risk of holding cash is increasing, and it is difficult to catch the exact bottom. Plus, you deserve to stop worrying about it.

- When, where, and why the current decline ends are difficult to know, but history tells us that stocks and bonds don’t go on sale by 20% more than about once every five years.

- Think back to what happened when the market bottomed after the Great Panic in 2009—the S&P 500 went up seven times in the next 13 years.

- When the market turns, it is sudden and sharp. Nobody rings a bell at the bottom.

- At this point in bear markets, the risk is less that you will get caught in the last 20% decline. The significant risk is that you get caught outside the next 100% advance, which would adversely affect most retirement plans.

- If you stay invested and the equity market goes down 20%, you may regret that for a few months. If the market runs away from you while attempting to time it, you’ll likely regret it longer. By far, the most potent emotion in investing is long-term regret.