Investment Shock Absorbers (Continued)

If you’ve ever taken a long road trip, you’ll know that conditions along the way can change quickly and unpredictably, which is why you need a vehicle that’s ready for the worst roads as well as the best. While diversification can never completely eliminate the impact of bumps along your particular investment road, it does help reduce the potential outsized impact that any individual investment can have on your journey.

[1] Adapted from “Investment Shock Absorbers,” Outside the Flags, February 2017.

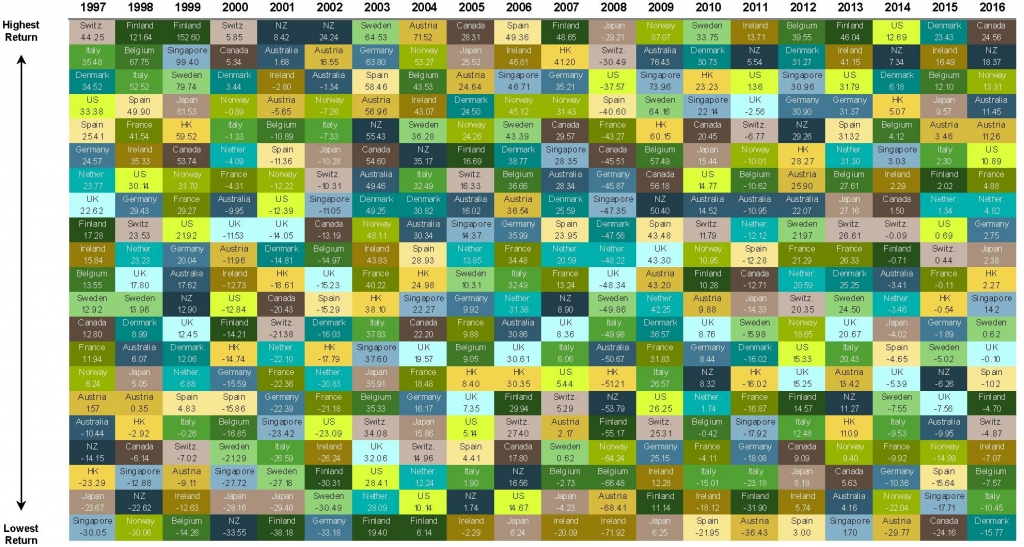

[2] In US dollars. MSCI developed markets country indices (net dividends).

[3] In US dollars. US Small Cap is the Russell 2000 Index. International Small Cap is the MSCI World ex USA Small Cap Index (gross dividends).

High Valuations Conundrum

Much research has been done on stock valuations, and historically buying into the market at lower valuations has seen higher returns than when buying in at higher valuations. However, the data is noisy.

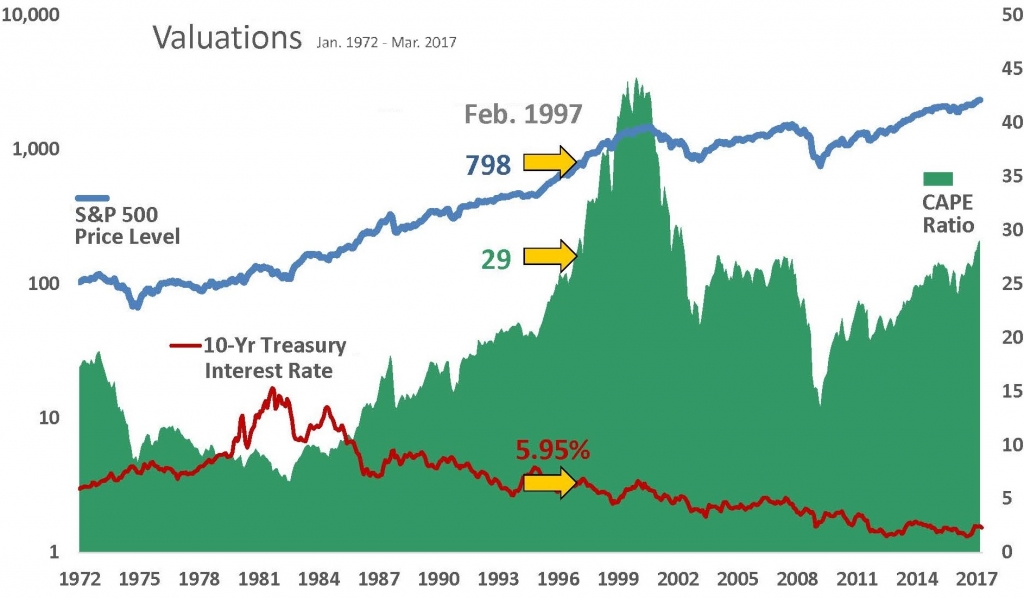

On the following chart, the green area represents the 10-year trailing price-to-earnings (P/E) ratio of the S&P 500, commonly referred to as the CAPE ratio. You can think of this as a gauge to see if the overall price of the stock market is expensive or cheap. As you can see, we’re currently at a fairly-elevated level, around 29 dollars of price for every dollar of earnings, though far below the peaks seen in 2000. [4]

It can be enticing to think it’s possible to time the market based on valuation ratios like these, but even the creator of this ratio, Professor Robert Shiller, cautions against using the ratio to make trades. And keep in mind you have to guess right not once, but twice — knowing when to get back into the market.

Take, for example, the last time the 10-year trailing P/E ratio of the S&P 500 broke through the current level was in February 1997. If you had sold out fearing high valuations at that time, you would have missed out on another three years of up markets, cumulating an additional 86% gain before seeing any meaningful decline.

At that point in February 1997, the S&P 500 was trading at 798; if you sold out waiting to buy back in once the market was lower, you would have had to wait twelve years, until March 2009. And if you missed that brief opportunity, you might still be waiting some 20 years later. Meanwhile, the S&P 500 is above 2,300.

Furthermore, it is important to note the level of interest rates over the last 20 years, as they are a major force on stock prices. A stock is generally valued by how much cash can be obtained from the company between now and judgment day, discounted by a benchmark rate. Many stock investors use the yield on the 10-year US Treasury bond as their benchmark rate, because it is assumed to be risk free and generally matches their investment time horizon.

In February 1997, the yield on the 10-year Treasury was 5.95%, and it has steadily declined since then, now standing at 2.38%, as of March 31, 2017. This might seem like a small change of only 3.57% (5.95% - 2.38% = 3.57%), but in percentage terms, it is a large 60% decrease (3.57% / 5.95% = 60%).

In the stock price equation, when the discount rate goes down, stock prices go up, and, at these levels, small changes in the discount rate can have a significant effect on an investor’s final valuation of a stock—this is just mathematics.

The difficulty arises in trying to predict the future scenario for interest rates. If an investor assumes these low levels of interest rates will continue for a long time, then stock prices look cheap, and they should buy, buy, buy. However, if an investor assumes interest rates will rise, then stocks start to look fully valued to expensive.

And both interest rate scenarios are a reality—for the low interest rate outcome just look to Japan over the last 30 years or the US in the 1940s, and for the high interest rate outcome look to the US in the 1980s.

Therefore, at TAGStone Capital, we recommend a balanced approach between stocks and bonds, with an appropriate rebalancing strategy, in case either scenario plays out. Instead of trying to predict what interest rates will be in three to ten years, we think a better strategy is to target dimensions of higher returns (size, value, and profitability) and stay the course when the market gets bumpy.

[4] Source: Robert Shiller Online Data library via Yale. CAPE tracks current S&P 500 price versus average of inflation-adjusted earnings over previous 10 years.