The Blueprint for Success

Now, let's revisit the essence of our planning and behavioral investment philosophy, which is remarkably straightforward:

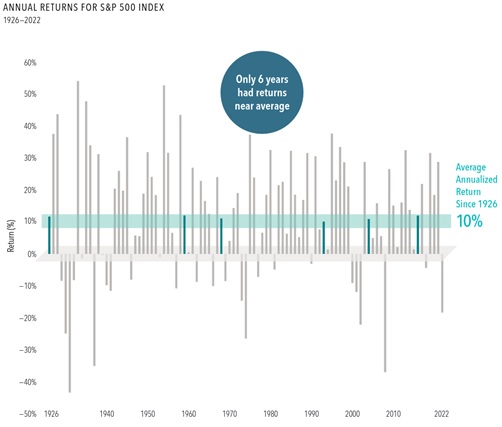

- Historical U.S. Equity Returns: A diversified portfolio of mainstream U.S. equities has historically delivered a compounded annual return of approximately 10% over the past two centuries, roughly 7% above inflation.[iii]

- Small-Cap Strength: Small-cap equities, due to their higher volatility and risk, have historically supplied average annual compound real returns of approximately 13%, roughly 30% higher than large-cap counterparts (around 9% versus 7% net of inflation). The volatility of small caps makes them ideal for long-term dollar cost averaging. However, ensuring that your exposure to small-cap equities is never so large that you might be compelled to sell them in a downturn is essential.

- International Exposure: The world economy is increasingly interconnected. International developed and emerging market stocks have delivered attractive compound annual returns averaging around 8.5% for the last fifty years, and they historically show less correlation with U.S. stocks.

- Bonds and Real Returns: High-quality corporate bonds, in contrast, have returned only about 3% above inflation over the same period, which is quite a bit less than half of the return of equities.

- Equity Returns Dynamics: The return gap between equities and bonds is because equity returns vary significantly above and below their long-term trendline in an efficient market (see exhibit below).[iv] While equity prices can decline considerably at times, these downturns, averaging over 15% per year since 1980 and roughly twice that on average one year in five since the end of World War II, have historically been temporary and eventually replaced by a long-term upward trend.

- Long-Term Positivity: Specifically, over the last century, approximately 75% of rolling one-year periods resulted in positive returns, a figure that increased to 88% over five years and an impressive 94% over ten years. Remarkably, there has not been a single rolling 20-year period in which equities produced a negative compound return.[v]

- Bonds as a Defense: While bonds play a vital role in a diversified portfolio, relying solely on bonds as a defense against temporary equity declines requires an investor to sacrifice more than half of the long-term returns historically offered by equities.

- Market Timing: The equity market cannot be consistently timed, just as the economy cannot forecast reliably. Therefore, the key to unlocking the full potential of equities lies in resolute, unwavering ownership through temporary declines—a skill possessed by only a small percentage of investors and often requires the guidance of a human investment advisor.

- Asset Class Choice: The critical long-term investment decision rests on selecting the broad ratio between equities versus bonds and cash, with the choice of individual securities holding less significance in the long run.

- Equity Diversification: Broad equity diversification is the preferred portfolio approach, dividing invested assets among funds with different styles, sizes, and geographical domiciles, which have historically run on different cycles.

- Rebalancing: Periodic rebalancing systematically reallocates capital away from sectors that have become overvalued toward those currently out of favor, potentially enhancing long-term returns. It is important to note that this approach differs from the actions of the majority of investors most of the time.