Staying Resilient in an Uncertain World

It’s hard to escape the noise these days—constant economic reports, market fluctuations, and political developments. We recently saw the S&P 500 drop over 6% in early August, with the CBOE VIX Index spiking to levels unseen since COVID. While unsettling, such volatility is not a reliable predictor of poor returns; historically, periods of high volatility often precede growth. Still, understanding this and experiencing it are two different things.

Success in investing—and in life—requires resilience. Nassim Taleb’s idea of being “antifragile”—thriving in adversity—is something to embrace. A solid plan feels reassuring in stable times, but it’s during downturns that the real test comes. Emotional intelligence, or EQ, counts just as much as knowing the numbers. By staying focused on your plan and tuning out the noise of temporary disruptions, you’re better positioned to see beyond the daily headlines and stay on track.

The Plan: Anchoring Your Strategy in Fundamentals

Knowing our natural tendencies, how do we build a resilient plan? Here are seven pillars to guide us:

- Align with Long-Term Goals: While maximizing returns is important, your portfolio should align with your family’s broader financial objectives. It should advance steadily, incorporating strategies like dollar-cost averaging, dividend reinvestment, and rebalancing.

- Trust the Plan Through Down Markets: Market declines are temporary. History shows that markets recover, and those who stay the course are rewarded over time. Believing in this and staying the course is crucial.

- Harness the Power of Compounding: Compounding is a quiet but powerful force in portfolio growth. The earlier we start, the more profound the effect. Consider two investors, one starting at 30 and the other at 40, both investing $10,000 annually. Assuming a 7% return, the early investor accumulates significantly more by age 65, underscoring the exponential impact of compounding.

- Rely on Equities for Income Growth: Equities don’t just build wealth; they also grow income. As businesses grow their earnings, they often raise dividends, which help protect against inflation. Since 1960, dividends on large U.S. stocks have compounded at nearly 6%, preserving purchasing power over time.

- Focus on Total Return: Dividends and interest are only part of the picture. Total return—capital gains plus income—is what ultimately drives wealth accumulation. Companies that reinvest in their business or buy back shares can increase their stock price, further building value.

- Minimize Taxes: Selling assets to avoid short-term volatility can lead to hefty tax bills. Short-term “paper losses” usually recover in a well-diversified portfolio, but you typically cannot recover the tax you paid on gains.

- Review Your Asset Allocation: With market valuations historically high, make sure your asset allocation aligns with your risk tolerance. If you’re overweight in stocks, rebalancing into bonds may be timely and help you avoid selling stocks during a market downturn.

Preparing for the Next Market Downturn

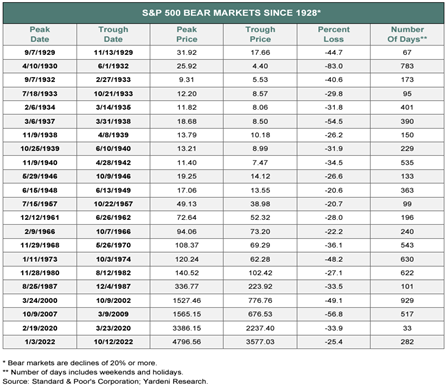

When markets are climbing, it’s easy to feel confident. But the real test—the one that separates speculators from investors—comes during downturns. Historically, large U.S. stocks see annual declines of around 15%, with steeper drops of 30% roughly every five years, and even a few major declines of 50% in the past 50 years. Yet over the long term, balanced portfolios have returned 6–10%, rewarding those who stick to their plan.

Each share you own represents a real business with employees, customers, and products. A downturn is simply a sale on these ownership stakes. Long-term investors see these periods as chances to acquire more of these businesses at a discount, confident that prices will eventually recover.

So, next time the market takes a dip, look around. Notice the steady hum of everyday life—the restaurants serving customers, the shops bustling with activity, the hotels with people still checking in. These reminders underscore that the world moves forward and that the companies we invest in continue to adapt and create value. In the long run, it’s those who stand firm and look for opportunity, not those who retreat, who come out ahead.