Do you ever listen to the news and find yourself thinking that the world has gone to the dogs?

The roll call of depressing headlines seems endless. But look beyond what the media calls news, and there are also a lot of things going right.

It’s true the world faces challenges in many areas, and the headlines reflect that. Europe has been grappling with a flood of refugees; as of May, the Chinese local A-share market declined by almost 20 percent; and the U.S. is in the middle of a sometimes-rancorous election campaign.

More recently, citizens of the United Kingdom voted to leave the European Union, creating significant uncertainty in markets over the long-term implications.

But it’s also easy to overlook the significant advances made in raising the living standards of millions, increasing global cooperation on various issues, and improving access to healthcare and other services around the world.

Many of the 10 developments cited below don’t tend to make the front pages of daily newspapers or the lead items in the TV news, but they’re worth keeping in mind on those occasions when you feel overwhelmed by all the grim headlines.

So here’s an alternative news bulletin:

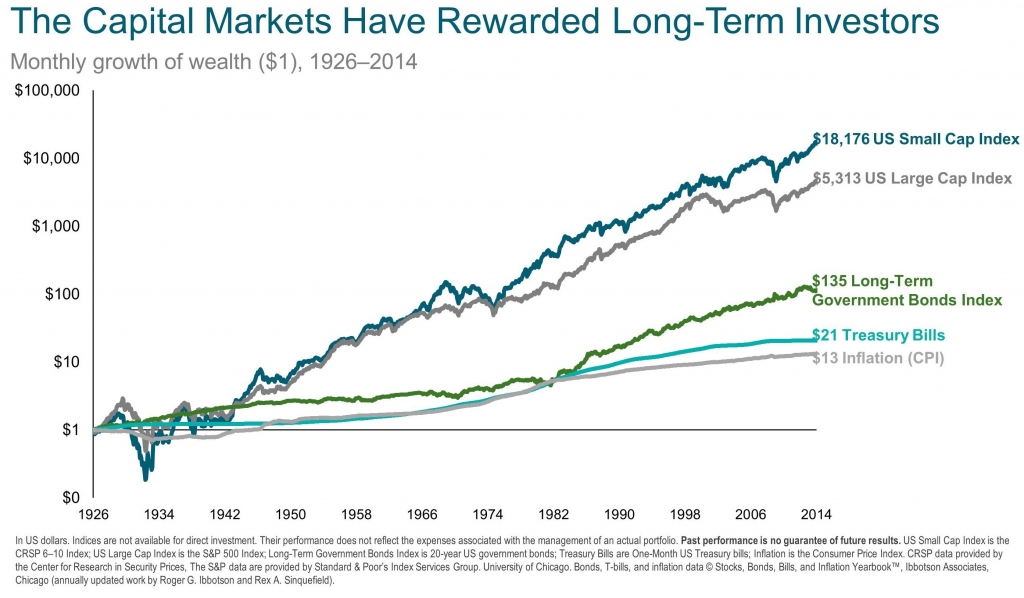

1. Over the last 25 years ending May 2016, one dollar invested in a global portfolio of stocks would have grown to more than five and a half dollars.1

2. Over the last 25 years, 2 billion people globally have moved out of extreme poverty, according to the latest United Nations Human Development Report.2

3. Over the same period, mortality rates among children under the age of 5 have fallen by 53%, from 91 deaths per 1000 to 43 deaths per 1000.

4. Globally, life expectancy has been improving. From 2000 to 2015, according to the World Health Organization, the global increase was 5.0 years, with an even larger increase of 9.4 years in parts of Africa.3

5. Global trade has expanded as a proportion of GDP from 20% in 1995 to 30% by 2014, signaling greater global integration.4

6. Access to financial services has greatly expanded in developing countries. According to the World Bank, among adults in the poorest 40% of households within developing economies, the share without a bank account fell by 17 percentage points on average between 2011 and 2014.5

7. The world’s biggest economy, the U.S., has been recovering. Unemployment has halved in six years from nearly 10% to 5%.6

8. The world is exploring new sources of renewable energy. According to the International Energy Agency, in 2014, renewable energy such as wind and solar expanded at its fastest rate to date and accounted for more than 45% of net additions to world capacity in the power sector.7

9. We live in an era of innovation. One report estimates the digital economy now accounts for 22.5% of global economic output.8

10. The growing speed and scale of data is increasing global connectedness. According to a report by McKinsey & Company, cross-border bandwidth has grown by a factor of 45 in the past decade, boosting productivity and GDP.9

No doubt, many of these advances will lead to new business and investment opportunities. Of course, not all will succeed. But the important point is that science and innovation are evolving in ways that may help mankind.

The world is far from perfect. The human race faces challenges. But just as it is important to be realistic and aware of the downside of our condition, we must also recognize the major advances that we are making.

Just as there is reason for caution, there is always room for hope. And keeping those good things in mind can help when you feel overwhelmed by all the bad news.10

[1] As measured by the MSCI All Country World Index (gross dividends) in USD.

[2] “Human Development Report 2015: Work for Human Development," United Nations.

[3] “World Health Statistics 2016,” World Health Organization.

[4] “International Trade Statistics 2015,” World Trade Organization.

[5] “The Global Findex Database 2014: Measuring Financial Inclusion Around the World,” World Bank.

[6] U.S. Bureau of Labor Statistics, 15 March 2016.

[7] “Renewable Energy Market Report 2015,” International Energy Agency.

[8] “Digital Disruption: The Growth Multiplier,” Accenture and Oxford Economics, February 2016.

[9] “Digital Globalization: The New Era of Global Flows,” McKinsey and Company, March 2016.

[10] Adapted from “10 Reasons to be Cheerful,” Jim Parker, Outside the Flags, DFA, June 2016.