By now, you’ve likely heard something about Trump Accounts — formally known as 530A accounts. They’re one of the more talked-about provisions in recent tax legislation, and for good reason: they’re a brand-new, tax-advantaged savings vehicle for children, launching July 4, 2026. For families thinking through Trump Accounts tax planning, the details matter quite a bit before you commit. Before your family rushes to open one, here’s what you need to understand.

What Are They?

Trump Accounts are a type of custodial account — owned by the child but administered by an adult until the child turns 18. Family members can open accounts online at trumpaccounts.gov or by filing IRS Form 4547. They’re designed to fill a gap in the planning landscape. Custodial brokerage accounts (UTMAs/UGMAs) allow families to invest for a child, but growth is generally taxable. A 529 plan offers tax advantages, but only for qualified education expenses. And while children can contribute to a Roth or traditional IRA, they need earned income to do so — something most young children don’t have.

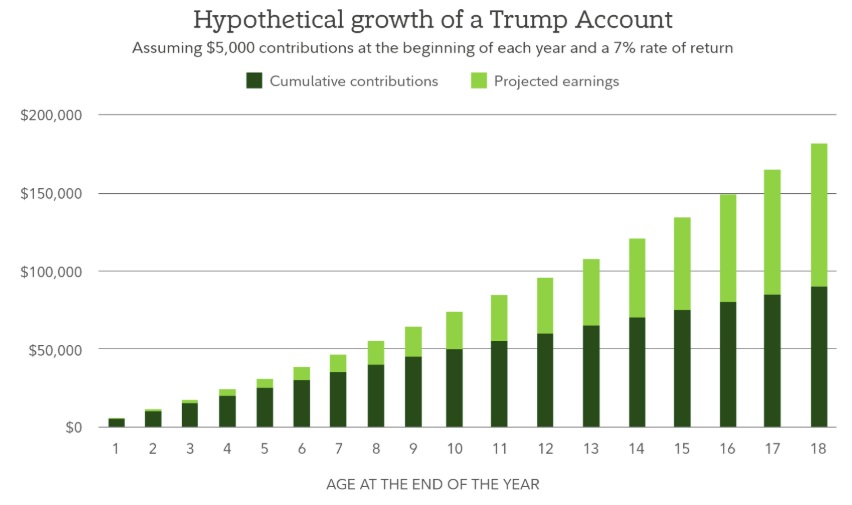

Trump Accounts require no earned income. Contributions of up to $5,000 per year can be made by parents, grandparents, adult siblings, legal guardians, or employers, as long as the child has a Social Security number and hasn’t yet turned 18 in the year the account is opened. Employers can also make matching contributions, which are deductible up to $2,500 and count toward the annual limit.

For children born between January 1, 2025 and December 31, 2028, there’s an added incentive: a one-time $1,000 federal seed contribution deposited directly into the account (and not counted against the annual cap). Separately, up to 25 million children age 10 or younger in lower-income zip codes may receive an additional $250 through a charitable contribution from the Michael and Susan Dell Foundation.

Investment options will be limited — likely a narrow menu of low-cost U.S. equity index funds, similar to the federal Thrift Savings Plan, with an expense cap of around 0.10%.

How Withdrawals Work — and Why It Matters

Withdrawals from a Trump Account are not allowed before the child turns 18. Beginning January 1 of the year the child turns 18, the account converts to a traditional IRA — subject to standard IRA rules, including a potential 10% early withdrawal penalty before age 59½.

Like a traditional IRA, growth inside the account is tax-deferred, and withdrawals are taxed as ordinary income.

That’s worth pausing on. A family that instead invested in a taxable custodial account (UTMA/UGMA) would likely see long-term growth taxed at capital gains rates — which, for most long-term investors, are meaningfully lower than ordinary income rates. So without additional planning, a Trump Account can effectively convert what might have been long-term capital gains into future ordinary income. That trade-off isn’t necessarily bad, but it’s not automatically a win, either.

Trump Accounts Tax Planning: The Age-18 Roth Conversion

Here’s where the planning story gets interesting — and where these accounts may offer a genuine advantage for families who think ahead.

Under Notice 2025-68, Trump Accounts are explicitly permitted to be converted to a Roth IRA once they become IRAs at age 18. That’s significant.

At 18, many young adults are in college with little to no income. If a child converts their Trump Account to a Roth IRA during a year when their taxable income is low, they may owe conversion taxes at a very low marginal rate — potentially 10% or 12%. Once converted, the account grows completely tax-free, no required minimum distributions apply during their lifetime, and withdrawals in retirement are income-tax free.

Used intentionally this way, a Trump Account becomes something closer to a delayed Roth funding mechanism for minors — one that doesn’t require earned income during childhood. That’s a genuinely useful planning tool.

The Kiddie Tax Caveat

There’s one important wrinkle families need to understand before assuming an 18-year-old college student can simply convert the account at a low rate.

The kiddie tax is a provision in the tax code that taxes a dependent child’s unearned income at the parents’ marginal rate, rather than the child’s own rate. It applies to children under age 19, and to full-time students under age 24 who don’t provide more than half of their own financial support.

A Roth conversion counts as income in the year it occurs. If a child is 18, in college, and still a dependent, the kiddie tax could cause a large Roth conversion to be taxed at the parents’ rate — potentially defeating much of the benefit.

The planning implication: the optimal time for conversion is likely after the child is working, financially self-supporting, and no longer subject to the kiddie tax. That might mean waiting until age 22 or 23 rather than converting the moment the account becomes an IRA. The account continues growing tax-deferred in the meantime, which softens the delay — but families should be deliberate about the timing.

How Trump Accounts Compare

| Account Type | Tax Treatment | Earned Income Required? | Use Restrictions |

| Trump Account (530A) | Tax-deferred; withdrawals as ordinary income (Roth conversion possible) | No | Cannot withdraw before 18 |

| 529 Plan | Tax-free for qualified education | No | Education expenses only |

| Custodial Roth IRA | Tax-free growth and withdrawals | Yes | IRA rules apply |

| UTMA / UGMA | Taxable (capital gains rates) | No | None |

What Should Families Do Now?

For eligible children born between 2025 and 2028, accepting the $1,000 government seed contribution is a straightforward decision — it costs nothing and gives the account a running start. Over 60 years at a 7% annualized return, that $1,000 alone could grow to nearly $58,000. Add $50 per month in family contributions, and the account could reach close to $550,000 over the same period.

Beyond that, the question of whether to make additional contributions deserves a closer look. The answer depends on your family’s overall tax picture, whether a deliberate Roth conversion strategy is part of your plan, and how the account fits alongside other savings vehicles like 529 plans and IRAs.

These accounts have real potential — but the advantage isn’t automatic. It requires coordination.

If you’d like to talk through how a Trump Account might fit into your family’s financial plan, reach out. We’re glad to help.

As with many new legislative programs, details are still being finalized — for a full legislative overview, the Congressional Research Service published a comprehensive summary in April 2026.