Periods of geopolitical tension can cause sharp market reactions and unsettling headlines.

Recently, events in the Middle East have escalated rapidly. On Feb. 28, the U.S. and Israel launched an attack on Iran, setting off a rapidly escalating conflict across the Middle East. Fighting has spread to other countries, bringing with it destruction and loss of life.

In addition to the humanitarian toll, the conflict is making economic waves globally. As of 2025, 20 million barrels of oil per day—about 20% of global consumption—traveled through the Persian Gulf. That traffic came to a standstill after the attack, and oil prices climbed swiftly.

These events have investors worried and markets reacting. In early March, the CBOE Volatility Index jumped to its highest level since the near bear market last April.

What Exactly Has Markets Concerned?

Investors worry that rising oil prices could slow the economy. Energy is a key input for transportation, manufacturing, and other activities. When oil prices spike, many industries face higher costs.

Investors are also concerned about inflation. Higher energy prices can lead to broader price increases. What’s more, many investors were hoping the Federal Reserve would lower interest rates to boost the economy. If inflation rises, the Fed may be less likely to do so.

Your Portfolio Is Built for Moments Like This

While the headlines are alarming, periods like this are not unusual in long-term investing. At TAGStone, portfolios are designed with the expectation that geopolitical events, economic shocks, and market volatility will occur from time to time.

It’s important to remember that your diversified investment portfolio is built to withstand moments like this.

For instance, your portfolio already includes allocations to U.S. and international stocks, bonds, and cash. The fixed income portion of your portfolio, in particular, can help provide stability when equities become more volatile, helping smooth overall portfolio fluctuations.

Within the equity portion of your portfolio, diversification also helps manage risk. Some sectors may struggle when energy prices rise, such as technology and consumer discretionary.[1] On the other hand, energy companies might benefit from rising prices, potentially helping offset losses elsewhere.

A diversified portfolio does not eliminate losses, but it can help reduce the magnitude of downturns compared to broad market indices such as the S&P 500.

It’s also worth remembering that much of your portfolio is invested for the long term. Short-term market movements can feel uncomfortable, but the assets that fluctuate most today typically are the ones you won’t need to draw on for many years. As a result, you may not need to change anything about your portfolio to respond to the current news cycle.

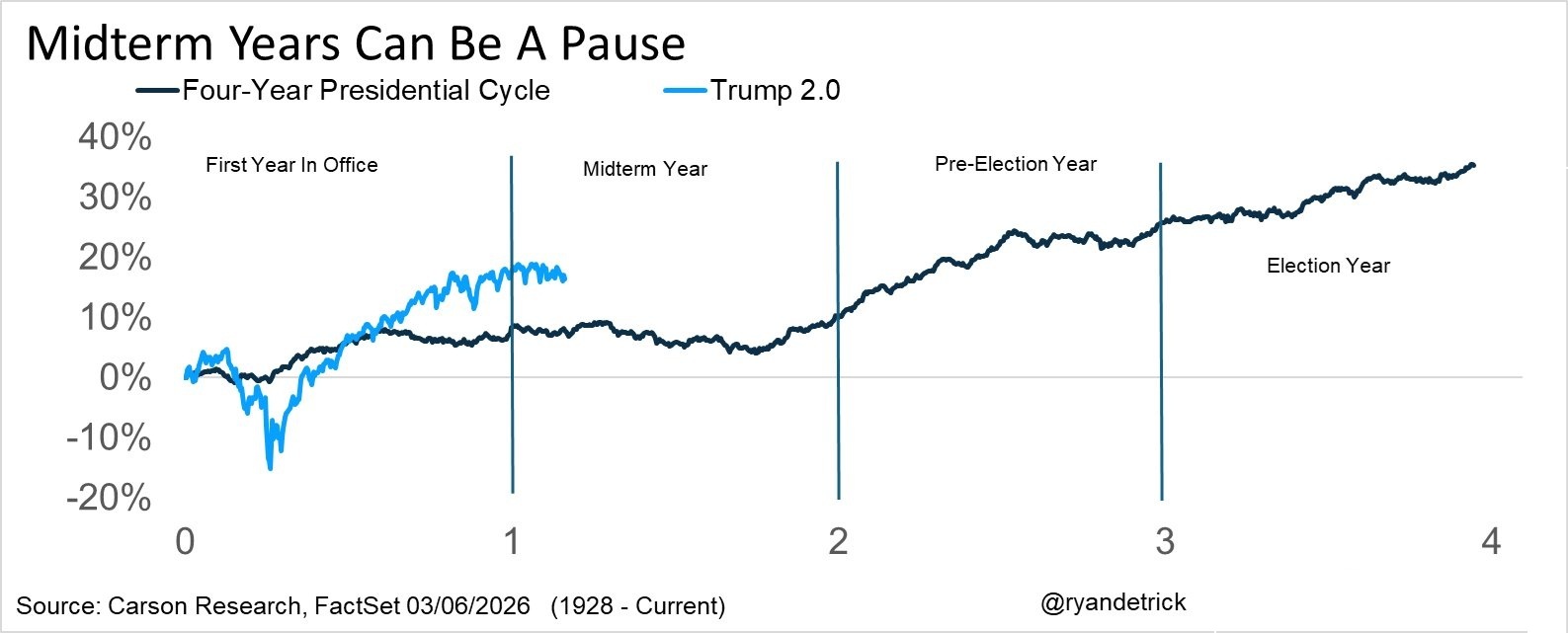

This year may also naturally bring somewhat higher market volatility. Historically, midterm election years have tended to experience larger intra-year declines—closer to about 17–18% on average versus roughly 14–15% in a typical year. While those declines can feel unsettling in the moment, the period following midterm elections has historically been one of the strongest stretches in the four-year presidential cycle.

A Final Perspective

In times of geopolitical crisis, it is natural for both people and markets to react quickly. History, however, suggests that these events rarely alter the long-term trajectory of markets.

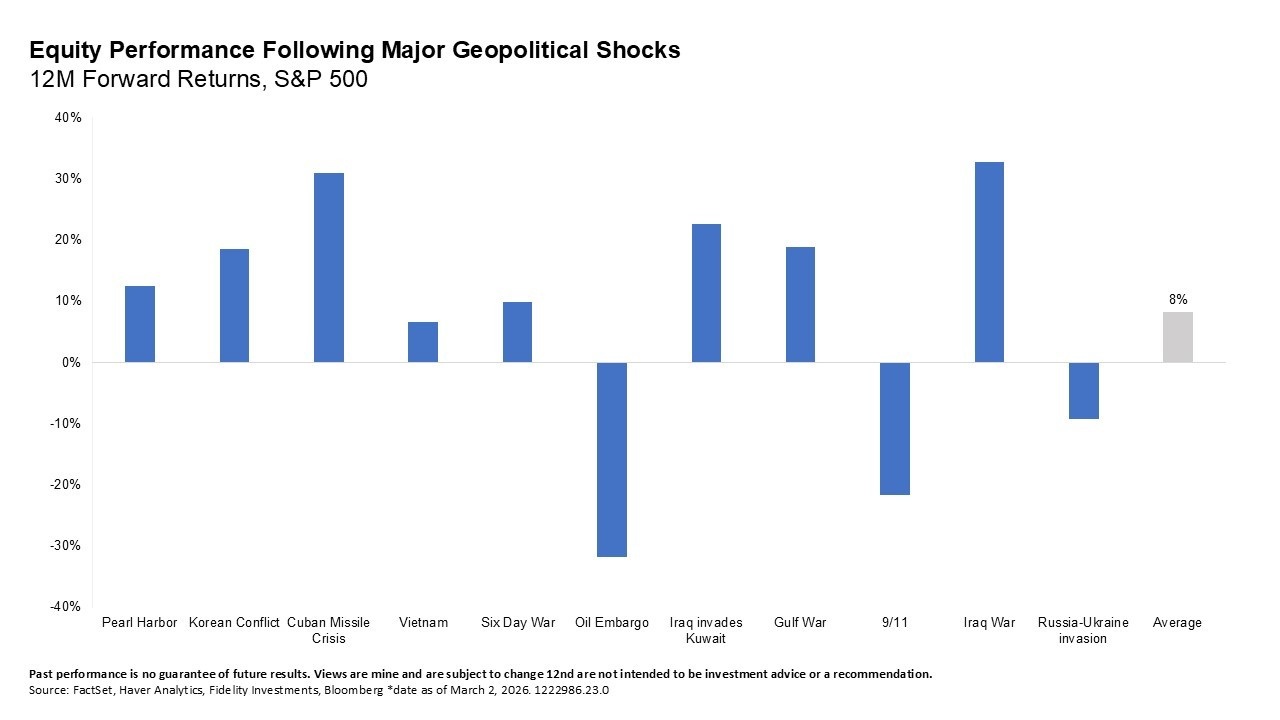

One useful way to think about geopolitical crises is that markets tend to treat them as temporary disruptions rather than permanent economic changes. Denise Chisholm, director of quantitative market strategy at Fidelity, looked into geopolitical shocks from Pearl Harbor through Russia’s 2022 invasion of Ukraine. She found that, on average, U.S. equities returned about 8% over the following year, on par with their long-term annual average. Her conclusion: “It’s the exception, not the rule, that geopolitical events become sustained market headwinds.”

The chart below illustrates how U.S. equities have historically performed in the year following major geopolitical shocks.

If you have questions about how current events may affect your portfolio, don’t hesitate to reach out. We’re always happy to talk through your concerns and help you stay focused on your long-term plan.

[1] See slide 6 of the linked chart pack.