Why Diversification—and Discipline—Still Drive Real Wealth

While the world debates how to invest in AI, the truth is simpler—and far more reassuring: you already own it.

Through a well-diversified portfolio of global businesses, you indirectly own hundreds of companies applying AI to become faster, smarter, and more efficient. From NVIDIA to Honeywell to Caterpillar, innovation isn’t a sidecar—it’s embedded in the very fabric of modern enterprise. And for long-term investors, the surest way to benefit from AI’s growth isn’t speculation—it’s ownership.

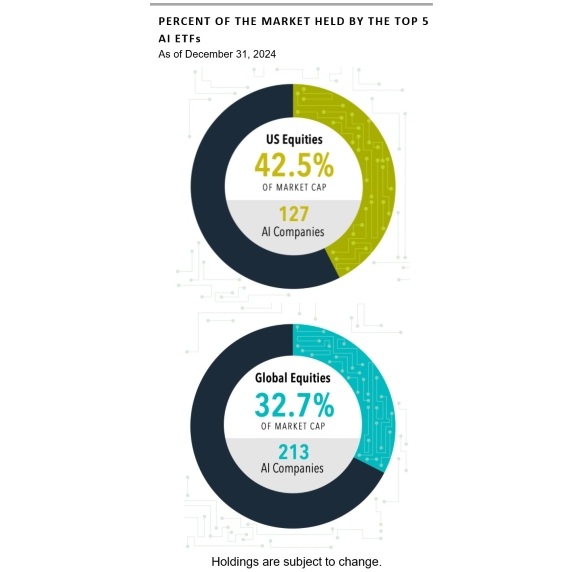

The rise of AI has inspired new funds and flashy tickers, but according to Dimensional’s research, the five biggest AI-focused ETFs (AIQ, BOTZ, QTUM, ARKQ, and ROBT) already include more than 40% of the entire U.S. stock market. Owning a broad, diversified portfolio already gives you exposure to hundreds of companies using or developing AI—you don’t need to chase new “AI-only” funds to benefit from the trend.

This underscores a comforting truth: investors don’t have to predict which company becomes the next great innovator. A globally diversified portfolio naturally captures the growth of AI and other technologies as they spread across industries. The winners of tomorrow are often found in places few expect today, from industrials and logistics to healthcare and finance.

Gold: The Eternal Mirage of Safety

This year, gold joined AI in the headlines, breaking record highs and rekindling old fascinations. Like AI, it stirs emotion. But unlike AI, gold doesn’t innovate, hire, or compound. It simply sits there.

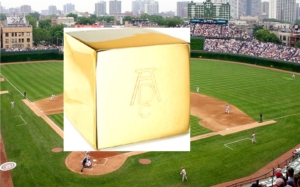

In his 2012 Fortune essay “Why Stocks Beat Gold and Bonds,” Warren Buffett imagined all the world’s gold—then about 170,000 metric tons—as a 68-foot cube that could fit neatly inside Yankee Stadium’s infield. At that time, the cube was worth about $9.6 trillion. For the same amount, Buffett wrote, one could buy every acre of U.S. farmland (roughly 400 million acres producing $200 billion a year in crops), sixteen ExxonMobils (each earning over $40 billion a year), and still have $1 trillion in “walking-around money.” The gold cube, by contrast, would just sit there. Buffett quipped, “You can fondle the cube, but it will not respond.”

Fast-forward to 2025. At $4,000 per ounce, that same cube—now around 212,000 metric tons—is worth roughly $27 trillion. That’s enough to buy every acre of U.S. farmland plus Apple, Microsoft, and Amazon combined—with change left over. Yet the cube still produces nothing.

If you own an ounce of gold for 100 years, you will still own one ounce at the end. That is its essence—its appeal and its limitation alike. It’s permanent, inert, and emotionally reassuring but financially unproductive.

History bears this out. In 1980, gold traded at $800 per ounce and has increased about 5× to $4,000 per ounce today. Contrast that with $800 invested in large-cap US stocks in 1980, which, with dividends reinvested, would have grown to $141,000, yielding a 176× total return and a 12% annual compound return.