Published May 5, 2026

At a Glance

- Disruption — tariffs, geopolitical shocks, pandemics — is a recurring feature of markets, not a new condition.

- Markets have historically absorbed shocks and recovered, but "long term" can mean a decade-plus (NASDAQ took 15 years to reclaim its dot-com peak).

- A diversified, properly allocated portfolio is built to weather these moments without reactive trading.

If it feels like the headlines have been relentless lately, that's because they have been. Over the past year, investors have had to process an ongoing trade war, sharp market swings and now the geopolitical shock of a war in Iran—all while trying to stay focused on their long-term financial goals. As we discussed in our Q1 2026 quarterly letter, economic news in the first quarter was dominated by the conflict in the Middle East and its effects on markets.

These are the kinds of disruptive forces that test our patience as investors. And while the current backdrop may feel uniquely unsettling, it's worth stepping back and asking: how does this moment compare to other periods of disruption? And more importantly, how should you respond?

Disruption itself is not new. It could come from government policy like tariffs, from geopolitical crises, from unexpected shocks like the Covid pandemic, or even from something as improbable as one of the world's biggest container ships blocking the Suez Canal for a week. History can give us a clue as to how events like these have shaken out—though, as the SEC likes to remind us, past performance is not indicative of future results. There's no way to know what will happen six days, six months or even six years after a disruptive event takes place.

What History Can Teach Us

Let's start with tariffs, since they've been a persistent feature of the economic landscape since early 2025. When the Trump Administration announced sweeping tariffs on Canada, Mexico and China—with rates ranging from 20% to 25% and climbing higher in subsequent rounds—markets reacted sharply. A series of stutter steps followed as the Administration alternately paused tariffs on some goods while increasing them on others.

History offers useful context. The Smoot-Hawley Tariff Act of 1930 is the most cautionary example: enacted during the Great Depression, it triggered retaliatory tariffs from Canada and European countries, contributed to a collapse in global trade and deepened the economic downturn. The first Trump Administration's 2018 tariffs told a different story—they didn't spark the same cascade, though they also didn't achieve their stated goal of reducing the trade deficit with Mexico, which actually increased by 159%.

As for the 2025 tariff round—we now have the benefit of hindsight. Markets absorbed the initial shock, experienced significant volatility and, true to form, began recovering as investors recalibrated. This is consistent with what more than a century of market history has shown: disruptions are painful in the short term, but markets have generally found their footing.

That said, it's worth being honest about what "long term" really means. The NASDAQ didn't reclaim its dot-com-era peak until 2015—15 years after the bubble burst. The S&P 500 delivered a negative annualized return for the entire decade from 2000 to 2009, underperforming both bonds and cash over that stretch. The long-term direction of markets has been upward—but the path can be grueling, and it can test even the most patient investors. This is precisely why a properly diversified portfolio matters as much as it does.

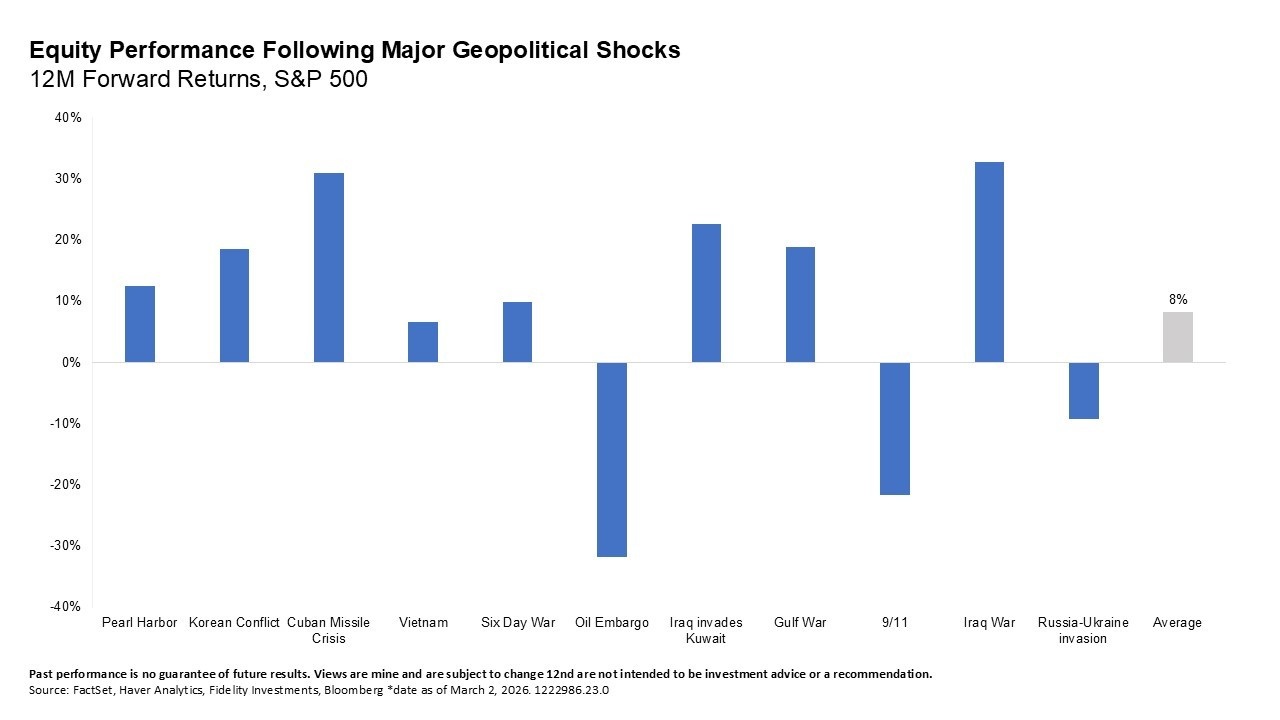

The same perspective applies to the Iran conflict that has dominated headlines in 2026. As we explored in When Geopolitics Rattle the Markets, geopolitical crises are unsettling by nature and their market effects can be sharp in the short term. But looking back at major geopolitical events over the past century—World War II, the Korean War, the Gulf Wars, the September 11 attacks—markets have ultimately found their footing, even when the recovery took longer than anyone expected.

Your Next Steps

None of this is to say that disruptions won't touch your daily life—they may. Rising prices from tariffs, energy market volatility from geopolitical conflict, uncertainty about future policy—these are real concerns that may warrant a closer look at your budget and spending, particularly if you're on a fixed income.

When it comes to your investment portfolio, though, remember that it's been designed with disruption in mind. Research shows that diversified portfolios—those that combine stocks, bonds and other asset classes—have historically experienced significantly less pain during downturns than all-equity portfolios, and have recovered more quickly as a result. Proper diversification and disciplined rebalancing are built to help you navigate uncertainty without having to make reactive decisions in the heat of the moment.

We've worked together to create an investment plan that's structured for tax efficiency and allocates your assets according to your need, willingness and ability to take on risk. If your goals or circumstances have changed, we can revisit your allocations. But if nothing fundamental has shifted, you may not need to make any changes to your strategy at all.

The noise can feel deafening right now. That's normal—and expected. Disruptions are, by nature, jarring. So if you have questions about what's happening in the markets, the economy or your own portfolio, please reach out. That's exactly what we're here for.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for returns and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources we believe to be reliable. However, some or all information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis do not agree.

The commentary contained herein has been compiled by W. Reid Culp, III from sources provided by TAGStone Capital, as well as commentary provided by Mr. Culp, personally, and information independently obtained by Mr. Culp. The pronoun “we,” as used herein, references collectively the sources noted above.

TAGStone Capital, Inc. provides this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult your advisor from TAGStone or others for investment advice regarding your own situation.