Hunkering Down in Turbulent Times

“What the imagination can’t conjure, reality delivers with a shrug.”

—Trumbo (movie voice-over)

Brace yourself. Your First Quarter 2020 report is likely to leave you feeling at least a little disheartened. No matter how much we’ve written about preparing for perilous times like these, planning for it versus actually enduring it is like watching a tornado on YouTube versus being swept into one in real life.

Yet, we stand by our advice. For emotional and financial turbulence alike, your best bet when you’re in the eye of a storm is to hunker down, and trust in preparations already made.

If you’re comfortable with how we’ve been managing your wealth so far, expect more of the same. As your steadfast fiduciary advisor, we will continue to help you implement the kinds of investment opportunities that make sense for you and your portfolio. These may include:

- Rebalancing your portfolio when warranted, to stay on course toward your long-term goals.

- Tax-loss harvesting where practical, to offset the costs of recently incurred and/or future taxable gains. (Yes, we still fully expect to see future market growth!)

- Roth IRA conversions when they may benefit your retirement planning.

- Seizing other opportunities when your plans call for it. For example, if you’ve been holding a concentrated stock position to avoid incurring taxable gains, now may be the perfect time to reduce your risks and strengthen your portfolio by selling all or part of that position.

A Stress Test for Your Risk Tolerance

If, on the other hand, you’ve begun to seriously question your course, think of current conditions as a stress test. Is the risk tolerance you thought you had holding up for you?

Ask yourself objectively: Can I tough out the fears I’m feeling right now? If so, we encourage you to stick with your existing investment allocations despite the angst.

What if you decide your portfolio is no longer appropriate for you? If that’s the case, let’s get together promptly to plan your next steps. Above all, your wealth should be structured to enhance your personal well-being. If that’s not what’s happening, we welcome the opportunity to help you adjust your portfolio accordingly.

Another question often asked during market extremes goes something like this: I’m okay with my portfolio mix, but why not get out of the markets temporarily until the worst is over?

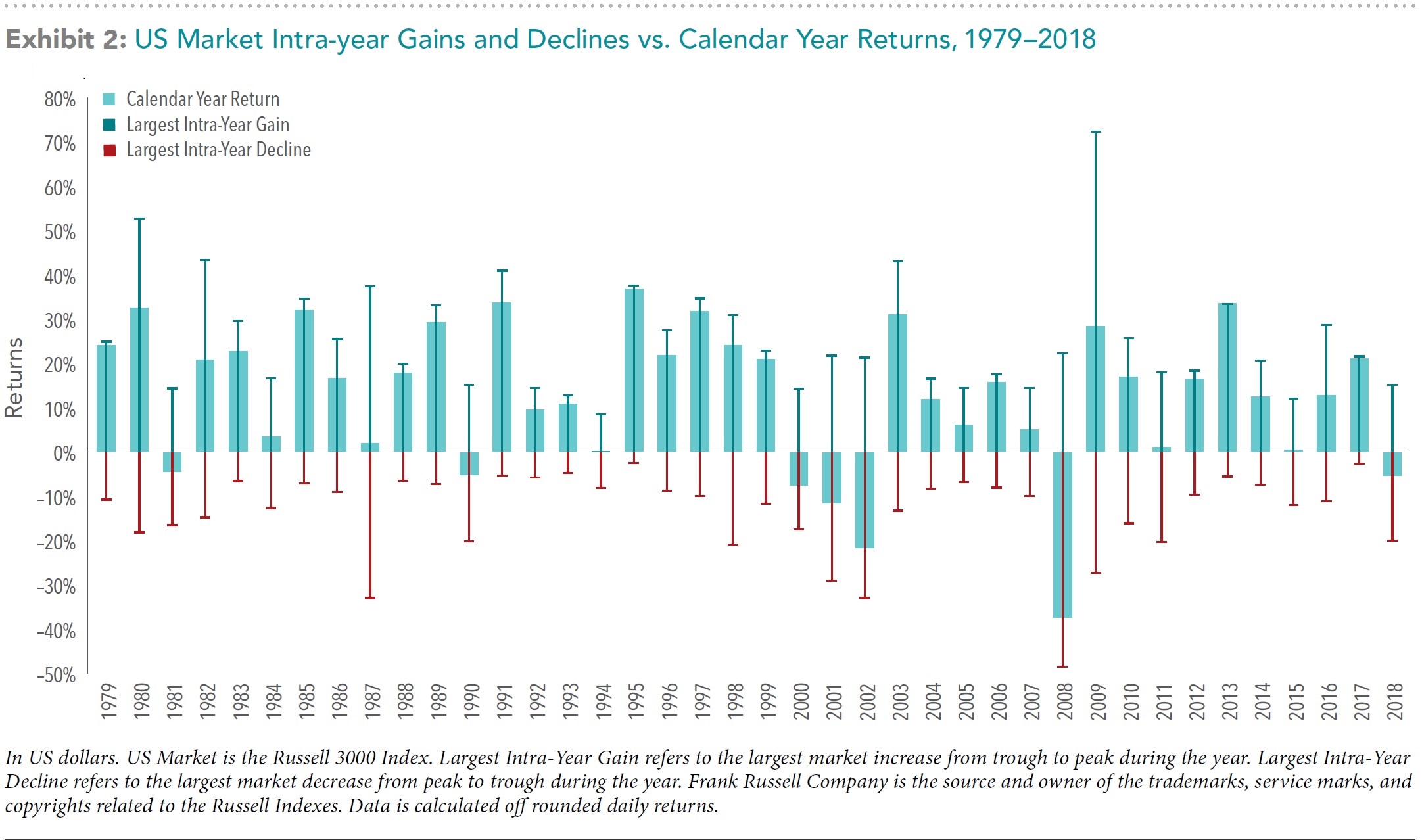

Recoveries Happen Quietly

Whether we leave your portfolio as is, or help you permanently reduce some of its risk exposure, we will never recommend trying to accurately time when to cleverly get out of, and safely jump back into volatile markets. While nobody knows exactly when a recovery will occur, history has informed us of what typically happens when it does. A recent Wall Street Journal piece explains, using the bull market that began back in 2009 as an illustration (emphasis ours)1:

"A surprising share of a new bull market’s returns pile up in its very early stages when people are most fearful. Take the one that ended last month. Putting $100,000 into an S&P 500 index fund on the day the bull began on March 9, 2009 and selling at last month’s peak would have seen that turn into $630,000 including dividends. Waiting just three months to make sure it wasn’t yet another head fake would have earned you only $450,000.”

In other words, while most of us are still assuming there’s no hope in sight, the markets can quietly and often dramatically make their big come-back … at least for those who have kept a portion of their wealth invested in them. The chart below shows the annualized return of the S&P 500 during eight recessions from the point when the bear market in stocks bottomed to when the recession ended in the real economy (i.e. stocks generally bottom several months before the recession ends).

Staying the Course

As always, without the ability to see what is only apparent in hindsight, we encourage you to focus instead on that which you can control. Right now, that is mostly doing all you can to keep yourself and your loved ones out of harm’s way. Please let us know how we can help.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for returns and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources we believe to be reliable. However, some or all information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis do not agree.

The commentary contained herein has been compiled by W. Reid Culp, III from sources provided by TAGStone Capital, as well as commentary provided by Mr. Culp, personally, and information independently obtained by Mr. Culp. The pronoun “we,” as used herein, references collectively the sources noted above.

TAGStone Capital, Inc. provides this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult your advisor from TAGStone for investment advice regarding your own situation.