Enduring Volatility: The Power of Patience in Investing

I am pleased to update you on our progress in the first half of 2024. Before examining the current market landscape, it is worth reflecting on what our disciplined approach has delivered so far.

Economic and Market Performance

The first six months of 2024 can be distilled into two key observations:

- Modest Economic Growth: The U.S. economy has continued to grow, albeit at a measured pace.

- Strong Equity Market Performance: The equity market has delivered impressive gains, driven by earnings growth and rising dividends.

We have seen steady economic growth, avoiding the feared recession, and job growth has held firm. Inflation has begun to ease, allowing the Federal Reserve to hold off on immediate rate cuts, although some are expected later this year. The Fed remains committed to its 2% inflation target.

Even with record-high cash dividends, large U.S. companies are paying out a smaller share of their earnings—about 37%—compared to the 30-year average of nearly 46%. This signals substantial potential for further dividend growth in the coming years.

Ultimately, the long-term value of our core investments—ownership in a diversified portfolio of successful companies—hinges on earnings and dividends. While external factors like national debt, elections, or geopolitical events can make headlines, the true drivers of value are the fundamental performances of the companies we invest in.

Recent Stock Market Volatility and Correction

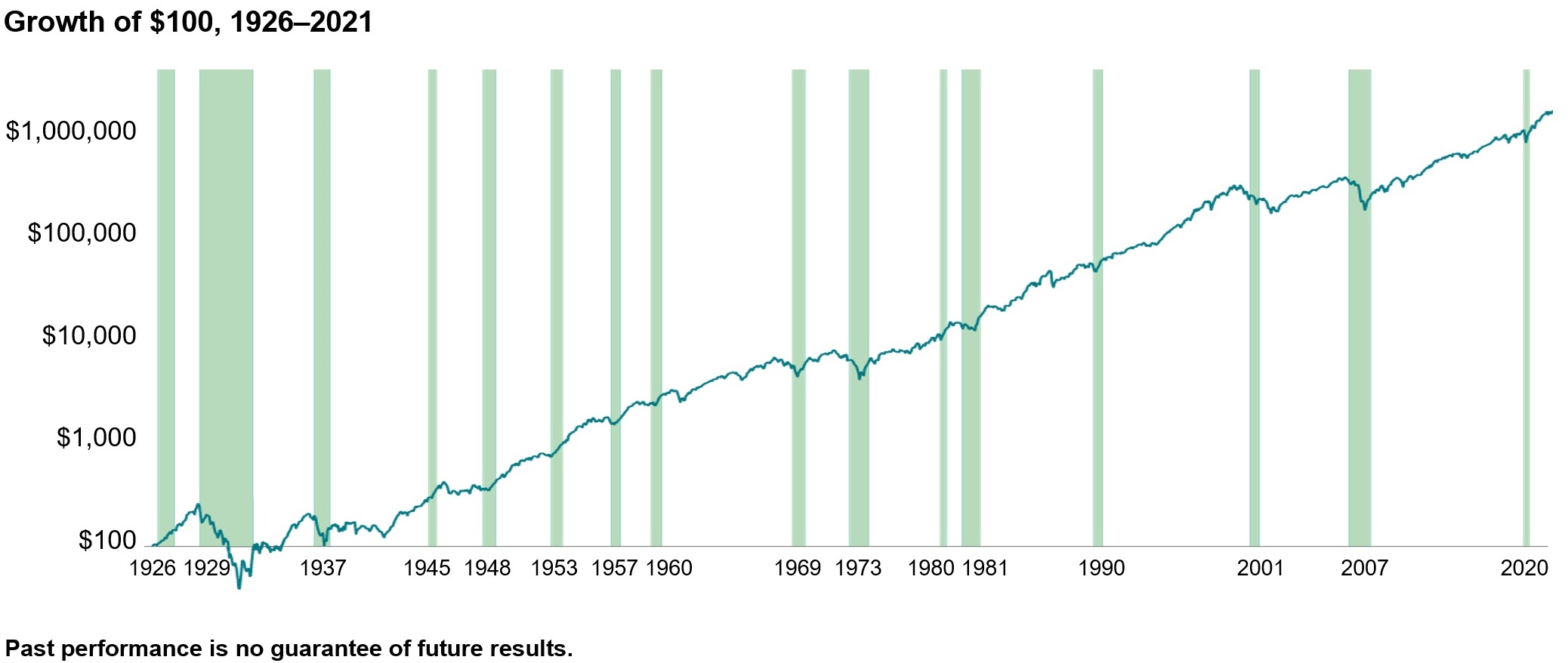

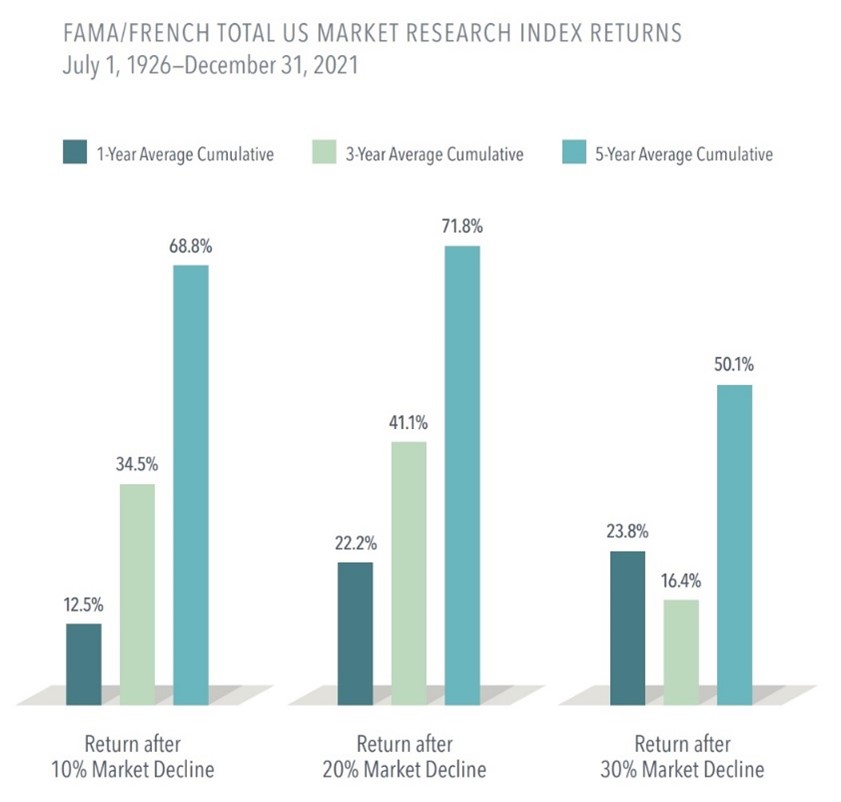

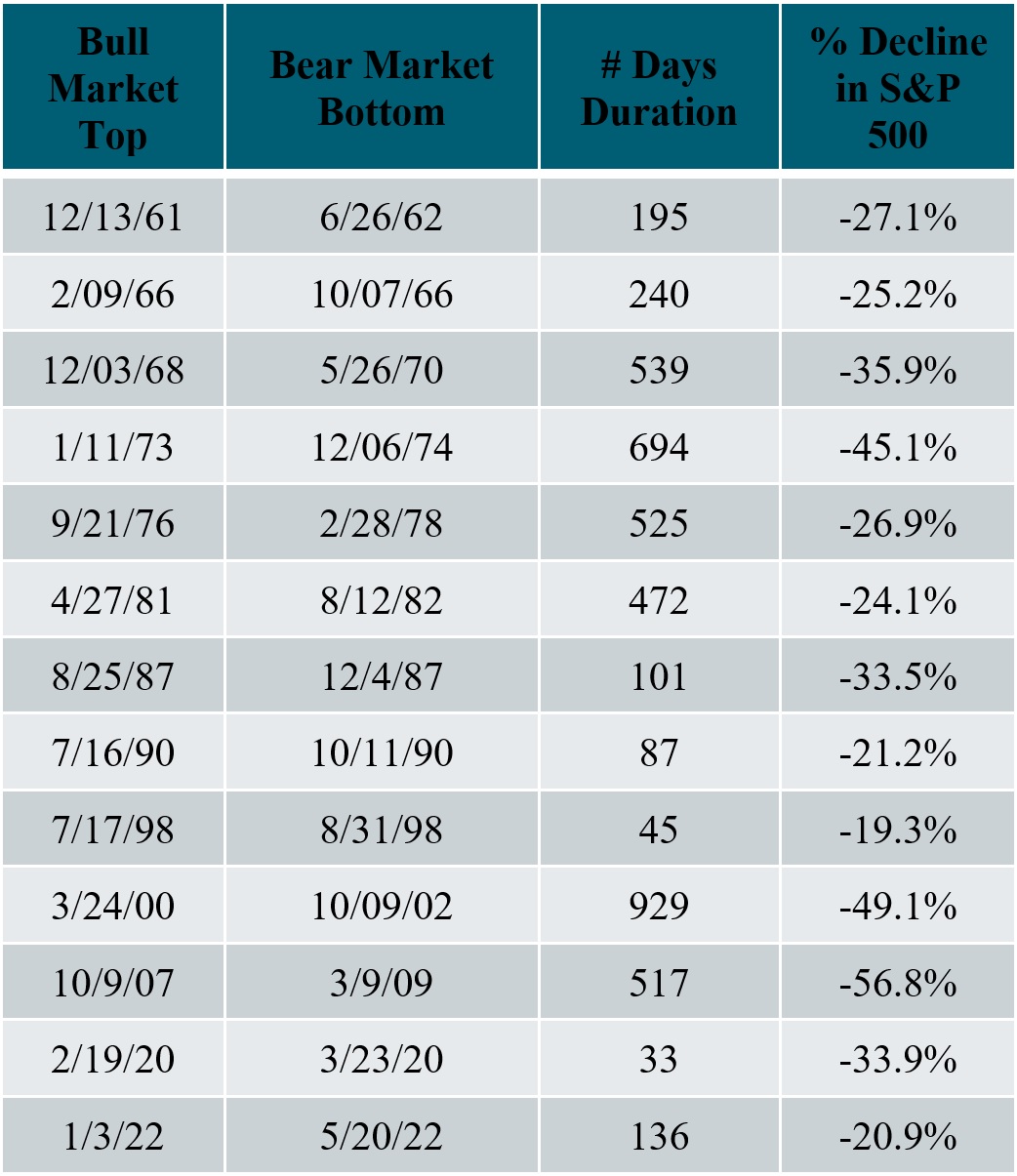

Since the close of the second quarter, we have seen the stock market go through one of its periodic bouts of volatility, almost dipping into correction territory after peaking on July 16th. A correction is typically defined as a decline of 10% or more from a recent high. While often unsettling, these events are hardly unusual—they happen roughly once a year. Our investment strategy, grounded in the principles of long-term value creation, is built to withstand these inevitable fluctuations.

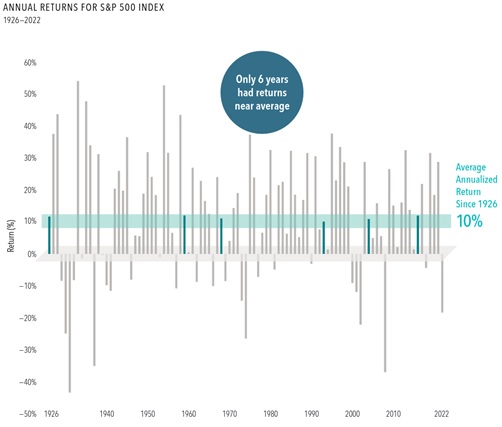

Historically, the average intra-year decline—the drop from the highest point to the lowest during any calendar year—has been 14.2% since 1980, reminding us that volatility is the price we pay for long-term gains.

While it's possible that this correction could deepen into a bear market (defined as a 20% decline or more from the peak), predicting the extent of a decline is a fool's errand. Historically, bear markets have occurred about every four years since World War II, with the last one ending in October 2022.

No matter what happens next, our long-term equity plan has proven its worth time and again. Here are the bedrock principles that guide our approach:

- Investing for the Growth of Purchasing Power: Our focus is on investments that grow wealth over time, even if they come with perceived risks. Holding cash may feel safer, but it’s a surefire way to lose purchasing power. The best tool for growing wealth is owning a diversified portfolio of successful companies for the long term.

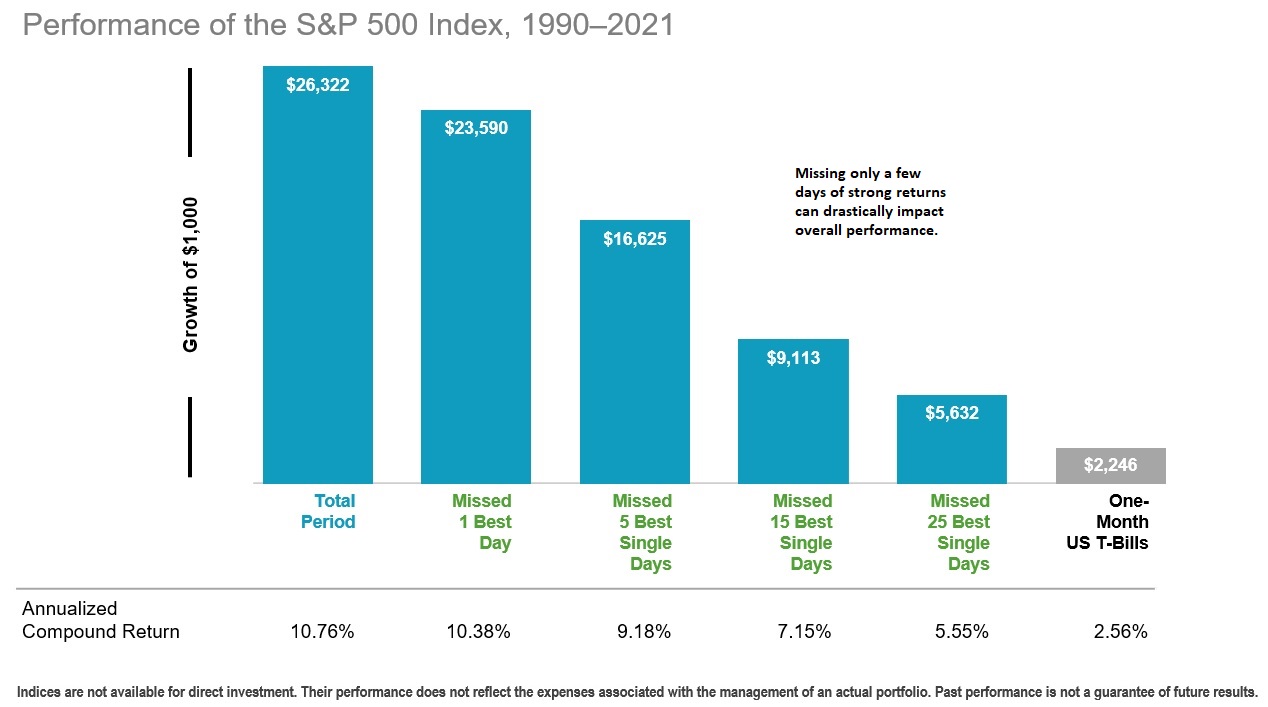

- Avoiding Market Timing: Trying to outsmart the market by timing one’s entries and exits is a losing game—especially after accounting for fees and taxes. The most reliable way to harness the full power of compounding is to stay fully invested.

- Seizing Opportunities in Market Downturns: We see market dips as opportunities, not causes for panic. Our strategy continues to work during temporary declines by reinvesting dividends and letting the power of compounding do its job. By purchasing more shares at lower prices, we amplify the powerful long-term benefits of compounding.

- Understanding Market Fluctuations: It is crucial to recognize that temporary declines in account value are not permanent losses of capital. They only become permanent when an investor sells out of fear.

- Rebalancing Periodically: Rebalancing involves trimming back asset classes that have grown beyond their target weight and reinvesting in those that have lagged, ensuring that your portfolio remains aligned with your long-term goals.

Political Turbulence and Investment Stability

It is natural to feel a bit on edge during an election year, with the usual mix of rhetoric and alarmism dominating headlines. With significant global tensions and nearly half the world’s population heading to the polls this year, the noise can seem even louder. However, history tells us that election outcomes have little to no meaningful impact on your long-term investment results.

One of the most persistent myths in investing is the belief that the outcome of the next presidential election will dictate market performance. Many people make short-term decisions based on election predictions, but countless studies have shown that neither the election result nor the occupant of the White House significantly impacts the long-term direction of the stock market.

Let us keep things in perspective with three key points:

- It does not matter much who the president is.

- The broad equity market goes up most of the time, regardless.

- The best course of action is to remain invested.

Never Interrupt the Compounding

The late Charlie Munger’s wisdom rings true as ever: “The first rule of compounding is never to interrupt it unnecessarily.” There is no greater unnecessary interruption than selling in anticipation of a presidential election. With election outcomes and the events of the next hundred days uncertain, our course remains clear:

None of this should concern lifetime investors. The strategy that has always worked is to follow a consistent, long-term plan. Presidents and their policies will come and go, as they always have. But through it all, superior companies continue to serve their customers, grow their earnings, and increase their dividends. At its core, investment success is almost entirely a matter of behavior.

Maintain a Balanced Investment Approach

Our investment philosophy is guided by your most cherished lifetime financial goals, not the ebb and flow of market conditions or economic forecasts. This perspective helps us counsel you toward making prudent financial decisions that favor long-term rewards over immediate gratification. Wise choices often mean delaying indulgence—like prioritizing life insurance over a luxury car, opting for disability insurance over a family vacation, or maximizing 401(k) contributions instead of purchasing a boat.

As financial interactions become more virtual, the value of personal, behavioral advice becomes even more critical. Working with a human financial advisor offers empathy, trust, and genuine connection—qualities that virtual platforms cannot replicate. Our role is to help you stay disciplined and focused on your long-term objectives, particularly when markets turn volatile.

In most areas of life, when prices drop, people flock to buy. When prices rise sharply, they cut back or seek alternatives. Yet, when high-quality equities fall in a bear market, panic often sets in, leading to a desire to sell. Conversely, when a particular stock sector or style surges, the impulse is to buy more of it.

Over a lifetime of investing, rebalancing should yield an incremental increase in your overall portfolio return. More importantly, regular rebalancing reduces positions in asset classes that have become relatively expensive (and potentially overvalued) while increasing positions in those that are relatively cheaper (and potentially more attractive).

The key is to remember that relative price and value are inversely related. Rebalancing forces us to embrace this principle, making us better long-term investors.

Broad diversification’s supreme goal is to spread risk. Once you have settled on the ideal allocation percentages across different asset classes based on your goals, rebalancing becomes a rational method to maintain that target mix while curbing the temptation to chase past performance.

The more we embrace our humanity and connect on a personal level, the more successful and valuable our relationship will be. As we wish you a happy summer, remember that we are here to help with any questions or concerns.

By focusing on the fundamental strengths of our core assets, we can tune out the noise and reduce the risk of emotional overreaction to market fluctuations. I believe in our plan and am confident in what we own.

Thank you, as always, for being my clients. It is a privilege to serve you.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for returns and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources we believe to be reliable. However, some or all information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis do not agree.

The commentary contained herein has been compiled by W. Reid Culp, III from sources provided by TAGStone Capital, as well as commentary provided by Mr. Culp, personally, and information independently obtained by Mr. Culp. The pronoun “we,” as used herein, references collectively the sources noted above.

TAGStone Capital, Inc. provides this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult your advisor from TAGStone or others for investment advice regarding your own situation.